Property in New Zealand and Australia

Property is much better value down under, finds Carla Passino

A kangaroo hops on a pure white beach, its silhouette dark against the vivid turquoise of sea and sky. Inland, sapphire waters carve deep fjords into white, vineyard-encrusted cliffs. And in the vast swathes of the Outback, the setting sun cloaks the dusty red of the desert in a rich palette of yellows, oranges and sienna.

The landscape alone would be enough to draw people to Australia and New Zealand, but good jobs, better wines and great, spacious properties spice up the mix, making the lure of living Down Under truly irresistible. ‘I've been to 100 countries around the world, but so far, Australia has been a real Land of Cockaigne,' believes Ghil'ad Zuckermann, who moved to Brisbane in 2004. ‘If you would like to move countries, I have no hesitation whatsoever: Australia is your destination. I cannot recommend it too strongly.'

Many people share his views. According to the Australian Bureau of Statistics, the country gains an international migrant every two minutes and 23 seconds. New Zealand doesn't quite match these heady numbers, but it still has a net immigration rate of 2.62%. And the British top the settler nationality charts in both countries, according to the 2006 census.

The prospects of finding a good quality, well-paid job are high among the reasons Britons flock Down Under both Australia and New Zealand have programmes favouring an influx of skilled migrants. Even better, settlers soon discover that their money will go a lot further here than it ever did in Britain. For example, says Prof Zuckermann, ‘academic salaries are very similar in Australia and the UK. Looking at purchasing power, however, the same amount of money buys much more in Australia than in the UK. And you usually get better quality'.

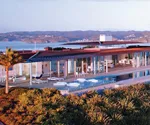

This is particularly true when it comes to homes. Properties in Australia and New Zealand come in a variety of architectural styles, from rustic 19th-century farmhouses to sleek ultra-contemporary villas, and they all tend to have plenty of space, views and vast plots of land. After all, there only are 2.6 Australians and 16 New Zealanders for every square kilometre against 246 people in Britain. Even better, buying one of these homes won't break the bank.

Prices have gently gone down in both Australia and New Zealand over the past 18 months, and this, coupled with historically low interest rates, makes prestige properties far more affordable than they were at market peak. In Australia, in particular, prices went down by 6.7% between the first quarter of 2008 and the same period in 2009, according to the Knight Frank Global House Price Index.

Behind this average figure, however, lies a three-tier market, where each price bracket experienced a different trend. ‘At the lower end, prices have risen between 5% and 10%,' comments Matt Whitby, director of research for Knight Frank in Australia. ‘The middle range (AU$500,000 to AU$2 million) has seen a relatively flat price growth; and at the prestige end (above AU$2 million), prices fell on average by 15%-20% since the peak in late 2007 and early 2008.'

The most exclusive houses those priced at AU$4 million or above performed worst of all, as the luxury sector bore the brunt of the credit crunch. Alex Caraco, CEO of Coldwell Banker Australia, estimates the average fall in this market segment to be at 30% to 40% since 2007.

Mr Whitby adds that ‘prestige prices are showing signs of stabilising'. Indeed, the latest Knight Frank index shows that Australian prices bounced back by 4.2% in the second quarter of 2009, and the annual drop over the same period in 2008 is now just 1.4%. This leads Mr Whitby to believe that ‘the window of opportunity for potential purchasers (particularly off-shore investors) seems to be closing'.

Over the Tasman Sea in New Zealand, ‘the property market seems to have been fairly lightly scathed by the economic recession,' according to Alistair Helm, CEO of industry website www.realestate.co.nz, who says: ‘In November 2007, median house prices peaked at $352,000, up from a 2001 figure of about $170,000. Since then, the median price has fallen and then recovered to be off the peak by just over 3% at $340,000. The lowest point was in January of this year at $325,000.'

Quoting figures from the Real Estate Institute of New Zealand and the local banking industry, Mike Bayley, managing director of Bayleys Real Estate, estimates drops to the tune of 13%-17% from the 2007 peak. Since last May, however, ‘there appears to have been a general stabilising and flattening out of the downward price correction,' he says. ‘This is partially attri-buted to a lower number of properties for sale on the market, which is constricting the supply and demand equation.

The corrections of the past 18 months have seen overpriced property return to more realistic values.' At the same time, however, ‘sales volumes collapsed midway through 2008 and fell to less than 50% of the previous year,' according to Mr Helm. ‘The total sales in 2008 were just under 56,000 units a far cry from the over 95,000 of the previous year and a peak of more than 120,000 in 2004.' The trend has affected all price brackets, although now that the first signs of recovery are rearing their head, top-end property is once again selling.

The jury is out among agents as to where the Australian and the New Zealand markets will go next. Some expect recovery to be well under way by 2011-12, but others think it may take longer. An optimistic Mr Caraco believes that ‘the Australian market has already commenced recovery' and could blossom in 2011 or even 2010, after the elections. He predicts prices will slowly rise in the next 12 months.

By contrast, Mr Whitby thinks Australia will see two parallel trends over the coming years. He expects activity at the lower end to reduce noticeably once the First Home Owners Grant a national scheme introduced in 2000 to help first-time buyers get a foot on the property ladder is phased out. ‘It will be up to developers and investors to take up the slack,' he says. ‘If this doesn't happen, we would expect to see prices top out and potentially fall at the lower end, as there was a mini-bubble forming there.'

On the other hand, he says, ‘we would anticipate the middle and higher ends to start recovering, particularly in inner-city locations, as demand still far outweighs supply, with strong population growth and not enough building activity.'

As for New Zealand, Mr Bayley believes ‘the market is close to bottoming out in terms of price corrections, if not there already, provided that factors such as unemployment levels, farming incomes and the exchange rate with the pound and the American dollar don't become unfavourable'.

And, although sale volumes will remain lower than average throughout the rest of 2009, they may well bounce back in the near future, thanks to New Zealand's natural shortage of stock, coupled with low interest rates and a favourable tax regime with no Capital Gains Tax. ‘This year will see some 75,000 sales,' Mr Helm says. ‘Perhaps, next year, we'll be up to about 88,000, and then by 2011, we may hit that long-term average of 95,000.' As a result, he predicts that ‘prices should hold up but not go wild'. In particular, he sees ‘potential for more top-end demand as a function of immigration.' After all, the lures of Australia and New Zealand are likely to outweigh and outlast any credit crunch.

* For more international property every week, subscribe and save